In our previous sessions, we have discussed the concept of profit sharing, how profits are recognised as income by the bank and how profits are distributed. The Writer shall now reveal the step-by-step profit calculation method using Microsoft Excel table (commonly referred to as "Profit Distribution Table) with Table/Chart examples, with the hope that ALL existing and potential users of Islamic banking system will be able to visualise how profits are actually distributed by Islamic banks.

It should be noted that the guidelines in calculating profits for distribution are stipulated in the Profit Distribution Framework issued by BNM (some of the terminologies used by the Writer may not be same as the framework) to ensure industry standard and one of the main items that BNM auditors normally audit in Islamic banks is Profit Distribution Table (PDT) records.

In most Islamic banks, the profit distribution table are prepared manually using Microsoft EXCEL but there are probably about three (3) Islamic banks (maybe) that have automated this process. The Writer opines that the PDT should be one of the items that Shariah Department and Bank's Internal Auditors should audit, since this process is still mostly done on manual basis thus open to possible calculation errors.

In Malaysia, there are two (2) profit distribution methods, namely;

(1) Weightage-Average-Ratio (WAR) Method, and

(2) Profit-Sharing-Ratio (PSR) Method .

The Writer wish to reiterate that this subject is very technical but the Writer will try to explain in the simplest way possible. Let us start this session with the WAR Method.

1. Weightage-Average-Ratio Method (WAR)

Under this method, the Bank will use various ratios known as the Weighted Average Ratio (WAR) for each deposit placement tenor (e.g. 3, 6, 9 months and so on) to represent the importance of one deposit tenor in comparison with another. For example, 12-month tenor deposit is considered more stable for the operation of an Islamic bank when compared to a 1-month tenor deposit. If a Customer places deposit for 1-month tenor, operationally the bank needs to monitor the deposit movement closely (especially for large deposits) as it does not have assurance that the 1-month tenor deposit will remain with the bank on maturity compared to a 12-month deposit tenor. Although depositor can still uplift the 12-month deposit prematurely, at least the bank does not have to worry about it for the next 11 months. Thus, to ensure fairness in term of profit distribution, depositors who place funds under a longer tenor deposit shall be paid higher profits (as required by Shariah) compared to those who place deposits under a shorter tenor. To do this, higher WAR will be assigned to a longer tenor deposits. Under WAR method, the profit sharing ratio (PSR) is fixed until maturity and if the bank decides to change the standard profit sharing ratio, it has to write to BNM with their justification (the Writer is not sure whether BNM has the rights to reject the request) and any changes on the PSR for existing accounts can only be affected on renewal. For automatic renewal accounts, consent must be obtained from the depositors.

Under conventional fixed deposits (FD), it is quite common where FD rates for longer tenor deposits are at times lower than the shorter tenor or vise verse depending on the deposit taking strategy of the bank thus, comparatively its more flexible compared to the Islamic bank WAR method. But if we are to look at it positively, conventional banks do not subscribe to the principle of fairness as compared to Islamic banks.

However, in practise there are still Islamic banks (perhaps 1 or 2 in Malaysia) that are not really following the principle of fairness mentioned earlier as the Writer observes that there are times when lower profit rates are declared for longer tenor deposit compared to shorter tenor. Perhaps, the bank is using the PSR Method where different profit sharing ratio is assigned for different deposit tenor. As for the PSR Method, most Shariah scholars are of the opinion that the principle of fairness does not apply since customer is aware of the profit sharing ratio for each type of deposit tenor before placing the funds i.e. element of offer and acceptance is presence prior placement of deposits. We shall discuss about the second method in details once we have examined the WAR Method.

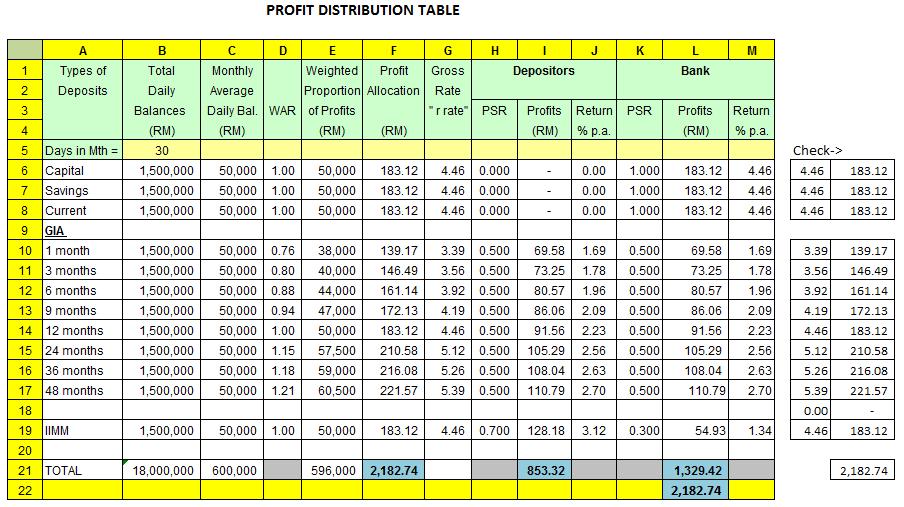

Now, let's see how profits is calculated using WAR method. At a glance, detailed view of the Profit Distribution Table is as per Chart 1 below.

Chart 1

Note: You can use zoom level of 150% to view Chart 1 clearly. The purpose of each columns will be clarified in next few charts as follows:-

Chart 2

Chart 2 can be explained as follows:

# Column A is the description of the various types of deposits (including other liability items) that are eligible to be included the PDT.

# Column B is the total daily balance comprising sum of daily balances for the whole month e.g. On Feb-1, the day-end balance is RM 50,000 while on Feb-2 the day-end balance is RM45,000. Thus, total daily balance for the first two (2) days is RM95,000. (Take note that to simplify our example, we are using RM50,000 as the daily day-end balance throughout the month). So, to get the total daily balances, system will accumulate the daily balances up to month-end. The month end total sum result will then be divided by the number of days in the month (for our example, we are using 30 days in the month) and that will give us the Monthly Average Daily Balances (MADB).

To understand the calculation, let's examine Chart 3 below:-

Chart 3

All the RM50,000 as shown in Column C of Chart 3 above, is the MADB for the respective tenor deposits. [Calculation for Line 10 Column A - RM1,500,000 divide by 30 or number of days in the month = RM50,000].

Now, how Weighted Average Ratio works? Let's examine Chart 4 below:-

Chart 4

# As earlier mentioned, the Weightage Average Ratio in Column D of Chart 4, is the ratio assigns to a particular deposit tenor to determine the importance of a particular deposit tenor compared to another. Under Column D, you will see that the WAR for 1-month tenor deposit is 0.76 while the WAR for 48-month tenor deposit is 1.21 and so on, as recommend in the BNM Profit Distribution Framework. As earlier mentioned, the WARs can be changed but the Islamic bank is required to inform BNM with their justification for changing the same.

# Thereafter, the AMDB of RM50,000 times the WAR of 0.76 will give us the Weighted Proportion of Profits (WPP) of RM38,800. What it means here is that although the original deposit amount is RM50,000 but for profit distribution purposes, the deposit placed with the Bank is treated as though it is only RM38,000 for profit distribution purposes. Likewise, for 48-month tenor deposit of RM50,000 with WAR of 1.21, the Weighted Proportion of Profits is RM60,500 [RM50,000 x 1.21 = RM60,500]

Once, all the WPPs are obtained for all types of deposit tenors, profits can now be distributed. For our example, let's assume gross income from operations is RM2,182.74 (refer to Chart 5 below)

Chart 5

What is Chart 5 all about? Simple understanding of the chart - Capital funds + Deposits equal to total deposits of RM600,000 for bank's operations. From the total deposit, we deduct statutory reserve (SR) , say 4% (RM24,000) and liquidity ratio, say 15% (RM86,000), that will gives us RM576,000 available for investment and financing activities.

We further assume bank's only financing account (without taking into BNM other requirements such as large financing, single customer limit etc.) is RM400,000. At financing profit rate of 7.50% per annum, monthly income to the bank is say, RM 2,465.75.

Whatever amount not used for financing purposes plus liquidity amount, totally RM176,000 will be placed in the Islamic Interbank Money Market (IIMM). At a IIMM average profit rate of 1.50% per annum, the bank earns RM216.99 for the month which gives us the amount of RM2,182,74 for profit distribution.

It should be noted that the gross profit to be distributed to bank and customer is after deducting allowed cost by BNM such as general provision, specific provision, commission and fees (as discussed earlier under Topic 23). Operating cost will be borne entirely by the Bank. Take note again that for above example, we assume GP is provided based on amortized basis i.e. full amount to be provided is divided equally over 12 months (max). In practise, whatever GP amount must be provided within the same year and some banks, provide GP based on their projected financing balances to avoid large provision amount that may impact their monthly profits. We shall discuss more on GP in later Islamic Accounting session.

Our next calculation is to get the gross profit before distribution. Before we go into details, let's take a look at Chart 6 below that shows the amount of profits to be distributed and how the same is converted into percentage as follows:-

Chart 6

The gross profit before distribution amount of RM2,182.74 will be placed in total column in the PDT (Line 19/Column F) and since we are using EXCEL formula, the profits will be automatically distributed upwards to the type of deposits and WPP amount assigned to it.

Now, let's see how profits are distributed. (refer to Chart 7 below):

Chart 7

To calculate the Profit Allocation amount, we take the WPP for 48-month deposit tenor of RM60,500 and divide the same with the total weighted proportion of profits (Line 19/Column E) amount of RM596,000 [ 60,500/ 596,000] times the gross profit amount of RM2,182.74, and that will give us RM221.57 [ (60,500/596,000) x 2,182.74 =221.57) ] profit allocation for 48-month tenor deposits. This means, although the placement amount for 48-month deposit tenor is RM50,000, since it is a long-tenor deposit with WAR of 1.21 and assigned-deposit amount of RM60,5000, profit sum of RM221.57 from the total RM2,182.74 is allocated.

So, before we show you further the steps to calculate the percentage, the Writer which to explain on why we MUST convert the amount distributed into a percentage instead of showing the absolute amount, say RM221.57.

Why we need to explain this..? Till today, there are still Muslims who said that the profits normally declared in "percentage form" is "riba" because it emulates the "interest-rate percentage" of conventional bank. The Writer wish to reiterate that for conventional bank, the end-result is actual rate represented by percentage (%) but for Islamic bank, the actual end-result is an absolute amount in figure. But to analyze and to compare the performance of each deposit types and also to compare Islamic bank's deposit performance against the conventional FD, we need to convert the end-result from absolute amount into percentage. Thereafter to convert the amount into percentage, we take the profit amount of RM221.57 divide by the original placement amount of RM50,000 x 100 (to convert to percentage) times [365 days in the year and then divide by 30 days in the month], that will give us a gross profit percentage of 5.39% as shown in Chart 7 above.

Take note that the gross or "R" rate ("R" actually means Reference or reference rate) for 12-month tenor deposit currently being by Islamic banks as the profit-sharing ratio negotiation benchmark for Islamic Interbank Money Market (IIMM). For this reason, the WAR for 12-month tenor is 1.0 (We will learn more on IIMM in later session)

Once we already obtained the gross profit before distribution for each deposit tenor, the next step is to distribute the profits according to the agreed profit sharing ratio. In Chart 8, the PSR is 50:50 (normally written as Depositors: Bank which means 50% for Depositors and 50% for Bank). The "R" rate for this example is 4.46 (Line 14 Column G).

How let's look at Chart 8 below.

Customers' profit is calculated by taking the gross profit amount of RM221.57, then times that amount with the profit-sharing ratio of 50% to give a return of RM110.79. To calculate the effective return in percentage to the Customer, we take the net amount distributed i.e. RM110.79 divide by the original amount (RM50,000) times 100 x 365 days and divide by number of days in the month, which is 30 in this example. That will give us a profit percentage of 2.70% per annum. Since PSR for the bank is also 50%, the bank shall also be allocated the amount of RM110.79 with profit percentage also at 2.70% per annum.

Chart 8

From Writer's own experience, it is important to explain to bank's management of Islamic subsidiary parent bank that the percentage 2.70% which is high (maybe compare to conventional FD rate of say, 2.5% prevailing at the time) does not mean that the bank is out-of-pocket in comparison with conventional FD at 2.50% per annum. Since the PSR is 50:50, when we pay depositor the rate of 2.70% per annum, the bank shall also be allocated with 2.70% per annum. Some people in the parent bank may misunderstood that Islamic bank is over-paying to their long-tenor depositors.

Now, how to know whether our calculation is correct? To counter-check, the total profits payable to depositors (RM 853.32) plus the total profits due to the Bank (RM1,329.42), will equal to the amount or gross profit before distribution i.e. RM2,182.74 as per Chart 8

THE ABOVE EXAMPLES ARE STEP-BY-STEP CALCULATION OF THE WEIGHTAGE AVERAGE METHOD but another method which is allowed by BNM is the Profit Sharing Ratio Method to be explained below.

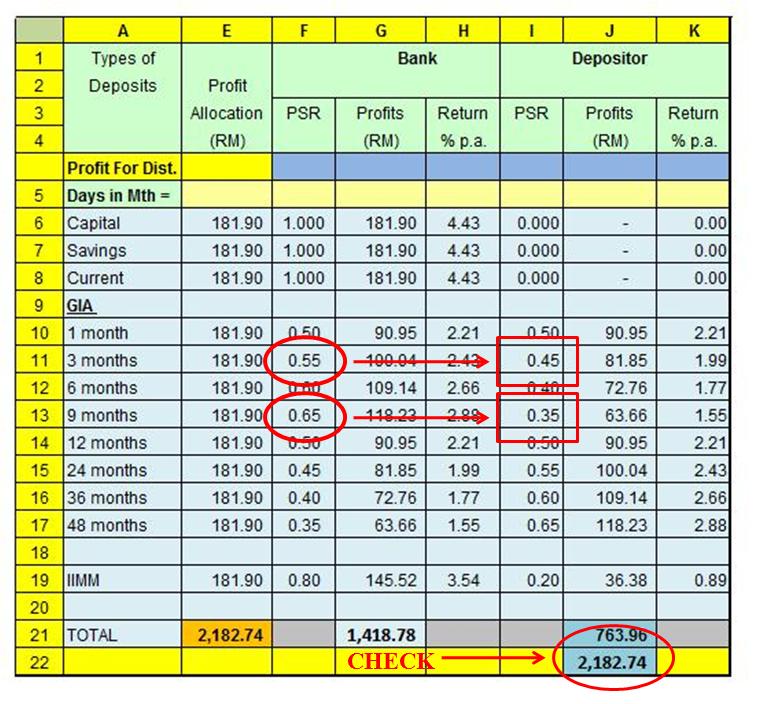

2. Profit-Sharing-Ratio Method (PSR)

The Profit-Sharing Ratio Method is the simplest method of profit distribution. The Bank will assign different profit-sharing ratios for the various deposit tenors. For example, for the same 18-month tenor, the profit-sharing ratio offered may be, say 80:20 (Depositor: Bank) in favour of depositors while for 24-month deposit tenor, the profit-sharing ratio may be 85:15.

Before we go into details, lets look at the overall PDT under the PSR method as per Chart 9

Chart 9

Now, lets' go into details (refer to Chart 10)

Chart 10

Unlike the WAR Method, under PSR Method, we need to determine the deposit volume percentage. This means, profits will be distributed based on the volume of each deposit type. So, based on our example in Chart 10 above, the Monthly Average Daily Balance of RM50,000 is divided by Total Average Monthly Balance of RM600,000 (Line 21/Column C) to get the percentage of deposit volume, which is 8.33% [50,000 /600,000 x 100 = 8.33% ]

Once the deposit volume percentage is obtained, we take the gross profit amount of RM 2,182.74 times 8.33% and that will give profit allocation of RM181.90 [RM2,182.74 x 8.33% = RM181.90 ]

Once we obtained the profit allocation, the same can be distributed immediately according to the profit sharing ratio for each type of deposit as per Chart 11 below:

Chart 11

Under the PSR method, the profit-sharing-ratio for longer tenor deposits can be lower than the shorter tenor. Since prior placement, depositor is made known on the profit-sharing-ratio, once the deposit is placed, the profit sharing ratio remains until the deposit matures. One very important advantage in using this method is that Islamic banks can response quickly to market demand on deposits. Islamic bank can raise the PSR immediately for new, say 1-month deposit tenor, if it needed large funds to meet sudden huge withdrawals. The bank can also offer varies PSR for different tenor deposits (refer Chart 12)

Chart 12

To check whether the PDT is correct, add the total amount to be distributed to the Customer and the profits due to the bank. If the amount is equivalent to the gross profit before distribution, the PDT is correct.

In order for Islamic Bank to gain better share of the profits, Islamic Bank will have to manage its deposit by offering lower sharing ratio to depositors e.g. using Tier-2 profit sharing ratio which means, if a Corporate depositor placed RM1.0 million under standard profit sharing of say, 50:50, any other amount above the RM1.0 million, the Bank may accept further deposits but at say, 60:40 (Bank:Depositor). This situation normally occurs when the market is flush with deposits.

This conclude our session on profit distribution and in our next session, we shall discuss on some related issues related to the Profit Distribution Table such as:-

1. Payment of profits - comparison between actual and maturity method. Why Islamic banks should use actual method;

2. Profit Equalisation Reserves;

Thereafter, we shall discuss about types of treasury products, Islamic Interbank Money Market and financing products.

Before we end this session, as promised for those who are interested to do some exercise on profit distribution Table, you may email to the Writer at

islamicbankway@gmail.com for profit distribution table exercise worksheet. In your request email, just let the Writer know your nature of business and your location (country) for the Writer's internal survey purposes according to the following category:

Student (country)

Conventional banker (country)

Islamic banker (country)

Legal Practitioner (country)

Shariah Scholar (country)

Non of the above (country)

IslamicBankingWay.Com

ALLAH KNOWS BEST.